Trigger warning: CRE winners and losers.

In every real estate cycle, some firms evolve, rebound, and thrive while others fall from grace, get acquired, or go away. Here's a relatively simple framework that can help to differentiate.

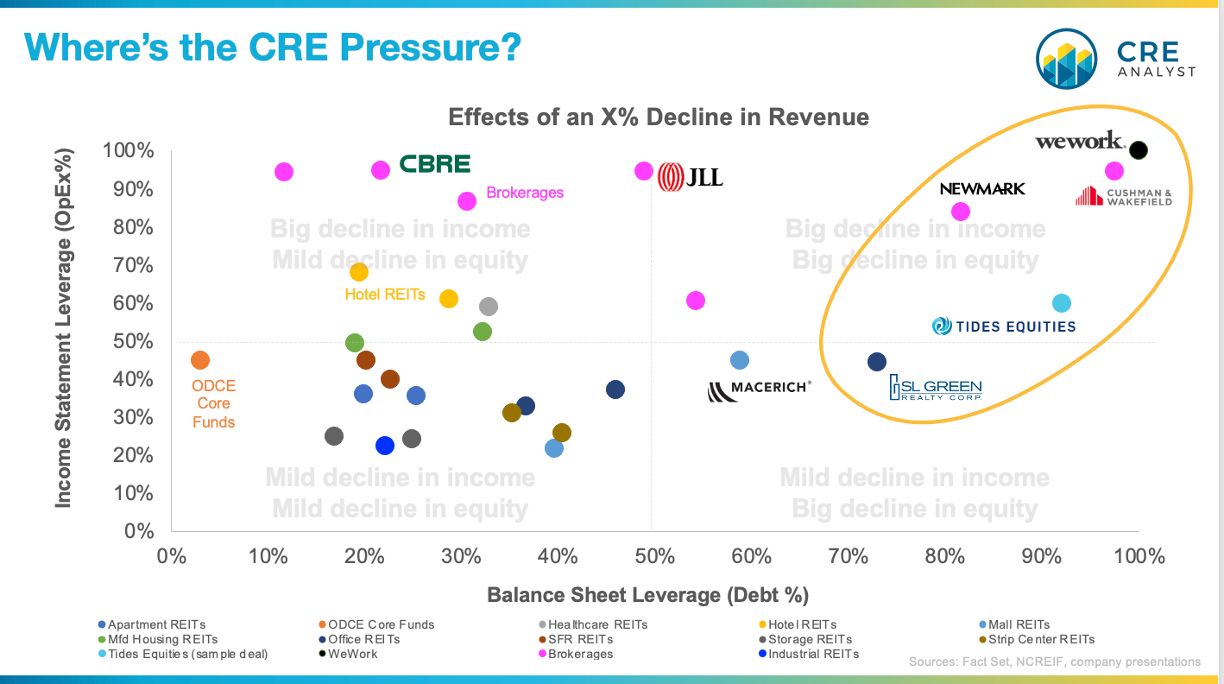

A company's ability to weather storms is largely a function of leverage.

-- Operational leverage: How sensitive is operating income to relatively small changes in revenue?

-- Balance sheet leverage: How sensitive is equity to changes in income? Firms that borrow a lot see more erosion of equity when income and value fall.

Combining these two components can often provide incremental clarity on sensitivity and resilience.

----- Our quick takes -----

From most sensitive (top right) to least sensitive (bottom left)...

1. WeWork: The options for WE are unfortunately very clear; renegotiate leases or go away.

2. Cushman and Newmark: Both would point out that their 'adjusted' leverage is lower. Fair point but we kept our figures consistent across brokerages. The fact remains: High expenses and relatively high debt with higher interest costs could make it difficult to deleverage and avoid cost-cutting in challenging times.

3. Tides Equities: We don't have company-level details but present Tides on North Plaza (a 420-unit property that was acquired in 2021 at a 3.5% cap rate) because we were able to get property information via securitization documents. Very limited flexibility.

4. SL Green: Falling stock prices and office values have increased balance sheet leverage, but the firm remains operationally efficient.

5. Macerich: Balance sheet leverage increased during the "retail apocalypse," but values have since rebounded, pulling balance sheet leverage back toward other REITs.

6. CBRE: Brokerage is a low-margin business (very different than building owners), but CBRE has more flexibility due to limited debt, which hides some prior missteps.

7. Hotel REITs: Very operationally leveraged (60-70 cents of every revenue dollar goes to opex vs. 25-35 cents in industrial, storage, and strip centers). Creates a clear need to cut in downturns.

8. ODCE Funds: Balance sheet leverage is likely understated by 10-25% due to inflated appraisals. Won't likely be active again until redemption queues moderate.

9. Storage REITs: Too much supply isn't great for revenue, but they are cash-generating machines with only 25% OpEx and very little debt.

10. ProLogis: Doesn't get any better in today's environment. Couldn't be more different than the financial crisis from a balance sheet perspective (much less debt now) and very operationally efficient.

Note: This analysis is inherently apples-to-oranges and for educational purposes only; the point of the chart is to demonstrate components of leverage across varied firms and structures. The charted figures are, in some cases, good-faith estimates based on publicly available information.

COMMENTS