Fool me once...

The brokerage model is pretty simple...

-- Hire talented experts

-- Support your brokers

-- Build a strong talent pipeline

-- Keep fixed costs low

-- Try to dominate a segment or geography

-- Ride the market's fluctuations

But sometimes brokerage firms get caught in a jam, typically due to...

-- Lack of revenue diversity

-- High fixed costs

-- Too much debt and/or ill-timed debt maturities

As cycles play out, strong shops tend to gobble up weaker ones via M&A or by hiring away their talent.

----- 3Q earnings update -----

We sift through brokers' quarterly earnings reports because they tell us a lot about market conditions. They can also reveal nuggets that separate winners and losers.

Here are our paraphrased summaries of the three brokerages that have reported 3Q23 earnings so far...

-- CBRE: 'Market stinks, slower recovery. Cost cutting. Maybe M&A but probably not; we'd rather keep buying shares to boost our bonuses.'

-- Cushman & Wakefield: 'Market stinks, slower recovery. We need to pay down debt and cut costs. May sell or recap some businesses to generate cash.'

-- Newmark: ‘Market stinks but light at end of tunnel. Expecting a rebound in 4Q23. Trimming costs to ease the blow.'

On deck: JLL and Colliers later today. W&D next week.

----- Biggest takeaways -----

Two common themes standout so far this earnings season:

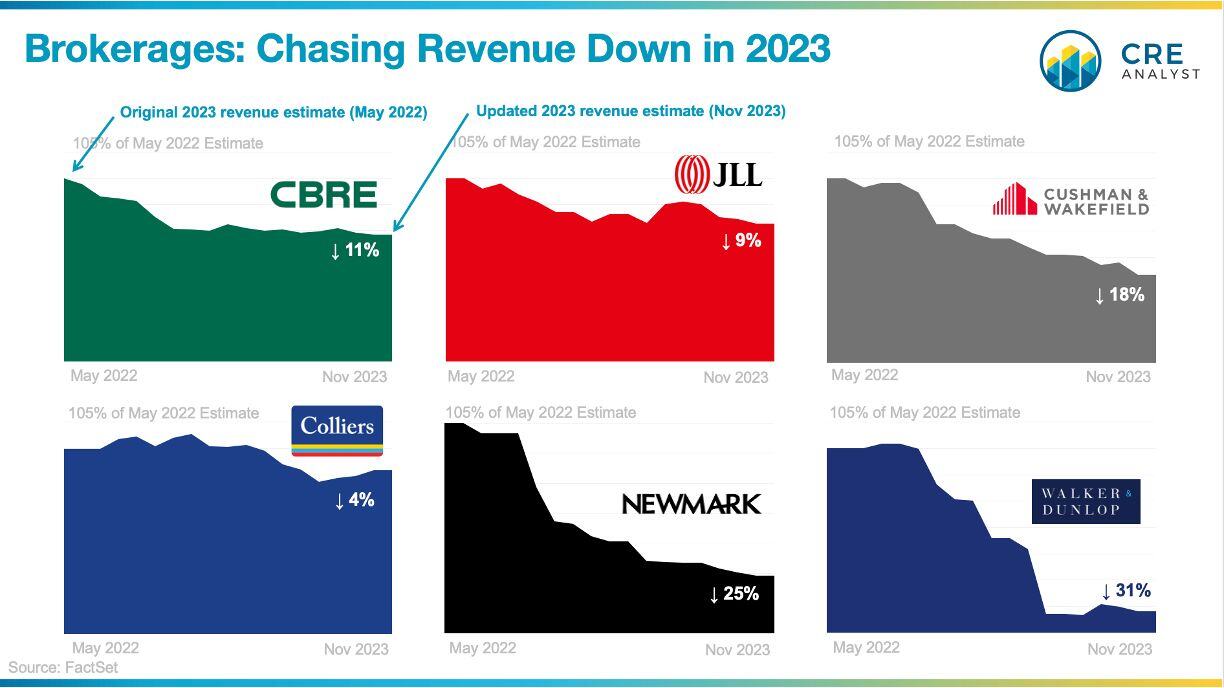

1. Continued downward revisions for 2023 brokerage revenue

18 months ago, sell side analysts expected 2023 revenues from the six brokerages we follow to come in around $77B, but now they expect revenues to come in around $68B.

Is it a surprise that brokerage revenues are down given the market's abrupt slowdown? No. However, it is a bit surprising that the same stimulus (slower transaction activity) is affecting brokerages very differently...

-- W&D is a pure play multifamily broker with very little revenue diversity, so its big decline isn't a huge surprise.

-- The revenue forecasts for CBRE, JLL, and Colliers were revised down in late 2022/early 2023, but they've been relatively consistent since the reset.

-- Newmark hasn't leveled off (yet), but the pace of decline moderated this quarter.

-- C&W seems to be on a steady decline.

2. Cost cutting

What do you do when revenue falls and interest expense spikes?

Cut expenses.

-- CBRE wants to cut $150M.

-- Newmark wants to cut $50M.

-- C&W is targeting $130M of cuts.

Note: C&W is 20% the size of CBRE in terms of revenue but has a cost cutting target that is nearly 90% of CBRE's.

When JLL and Colliers report later this morning, we'll have a clearer view of downward revenue surprises, delayed recovery expectations, and/or more cost cutting.

More to come...

COMMENTS