This case study has it all: Blackstone, Goldman Sachs, Class A apartments, Class B apartments, workforce housing, a $1.3 billion floating-rate mortgage, a near-term maturity, LTV > 100%, DSCR < 1.0x, and a springing interest rate cap.

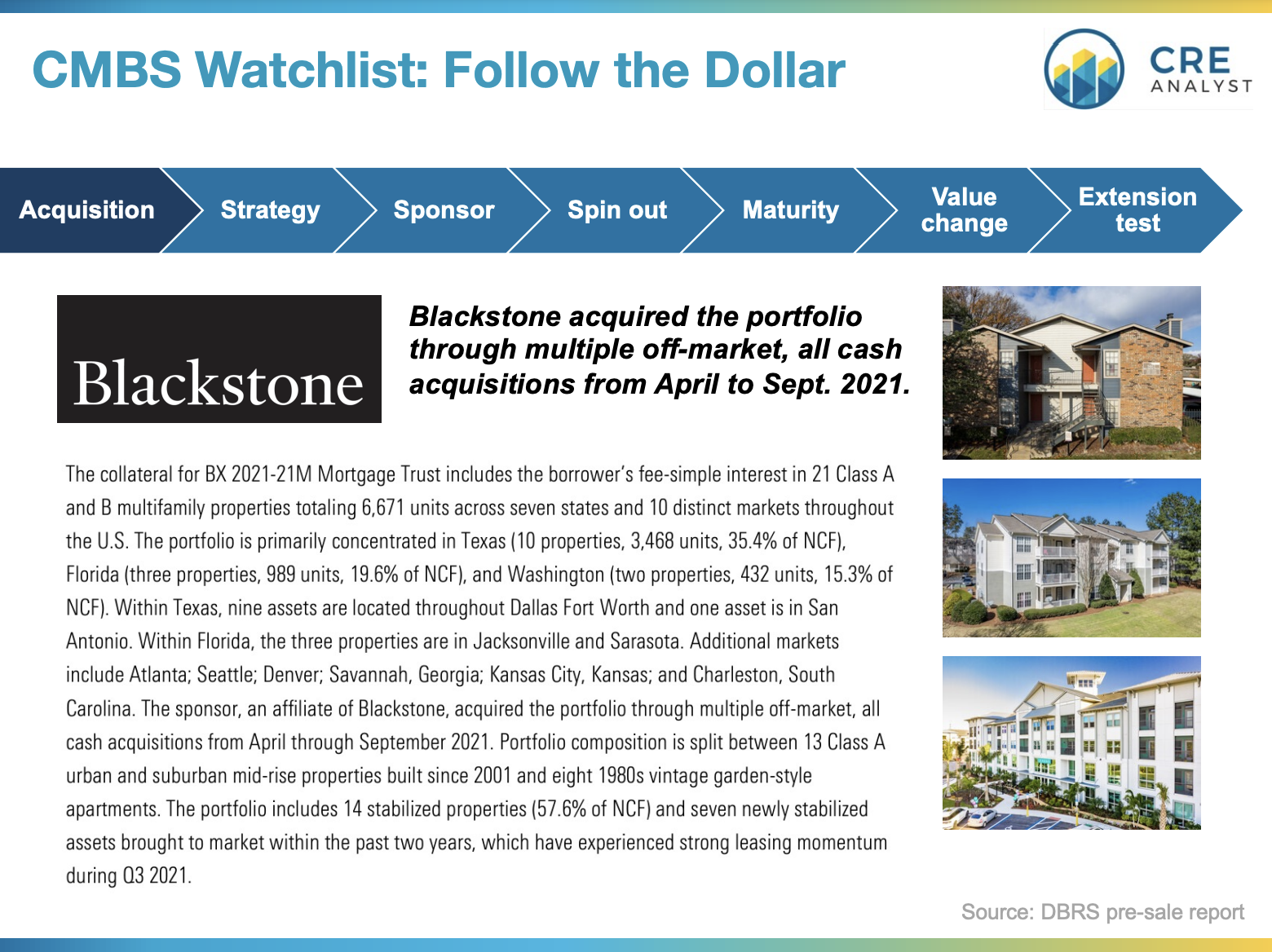

TWO YEARS AGO Blackstone was in the early days of BREP IX. With $20B of dry powder, the firm was gobbling up recently-completed Class A apartments and older Class B apartments in need of freshening up. ...off-market and all cash.

THANKS, MR. POWELL: The Fed stoked the post-COVID fire by buying $4-5 trillion of Treasuries and MBS, which pushed down interest rates and flooded the market with capital looking for yield. Blackstone was in the middle of aggregating their apartment holdings at 6% cap rates, when interest rates fell from 4% to 2%, pushing apartment cap rates below 4%.

SASB COMIN' IN HOT: Blackstone brought 6,700 units (20 years old on average) to the CMBS markets for debt in late 2021. With a strategy of leasing up and sprucing up units, pushing rents, and riding the cap rate wave, Blackstone opted for a single-asset single-borrower (SASB) securitization with a floating interest rate (the initial coupon was about 2.4%) and a two-year term. Blackstone borrowed $1.3 billion at 81% LTV, which was pretty high but at least had a DSCR of about 2.0x.

SELLING DOGS: About a year into the loan term, in late 2022, Blackstone sold about 2,800 units (all older, Class B product in Texas) to a Goldman Sachs partnership with a workforce housing focus, leaving BX with about $970M of debt secured by its remaining properties.

NEW RATES, NEW VALUES: Despite strong income growth at the remaining properties, debt service coverage tanked with spiking interest rates. Blackstone's original 2.4% mortgage coupon quickly turned into 7.4%; property cash flow doesn't cover annual debt service, which (on the entire $1.3B loan) ballooned from $32M to $97M. Also, values have fallen by 20%+ (per Green Street) since the SASB origination, which leaves Blackstone looking at a $970M maturity in Oct 2023 on a portfolio worth about $920M.

NEW RATE CAP REQUIRED: Blackstone has a few loan extension options with no performance tests. However, BX would have to renew its interest rate cap, which would cost about $27.5M. Will Blackstone throw in an extra $27M to extend? The firm could also pay down debt, but this seems unlikely; why would an opportunistic fund that targets 18%+ returns earn < 8% on those incremental dollars? Tossing back the keys seems like a better option.

YOUR CALL: Will Blackstone pay to kick the can or send the keys to the special servicer? Either way, this situation seems to capture many of the stresses defining today's real estate market.

Feel free to highlight any other case studies you think might be interesting for future posts.

COMMENTS