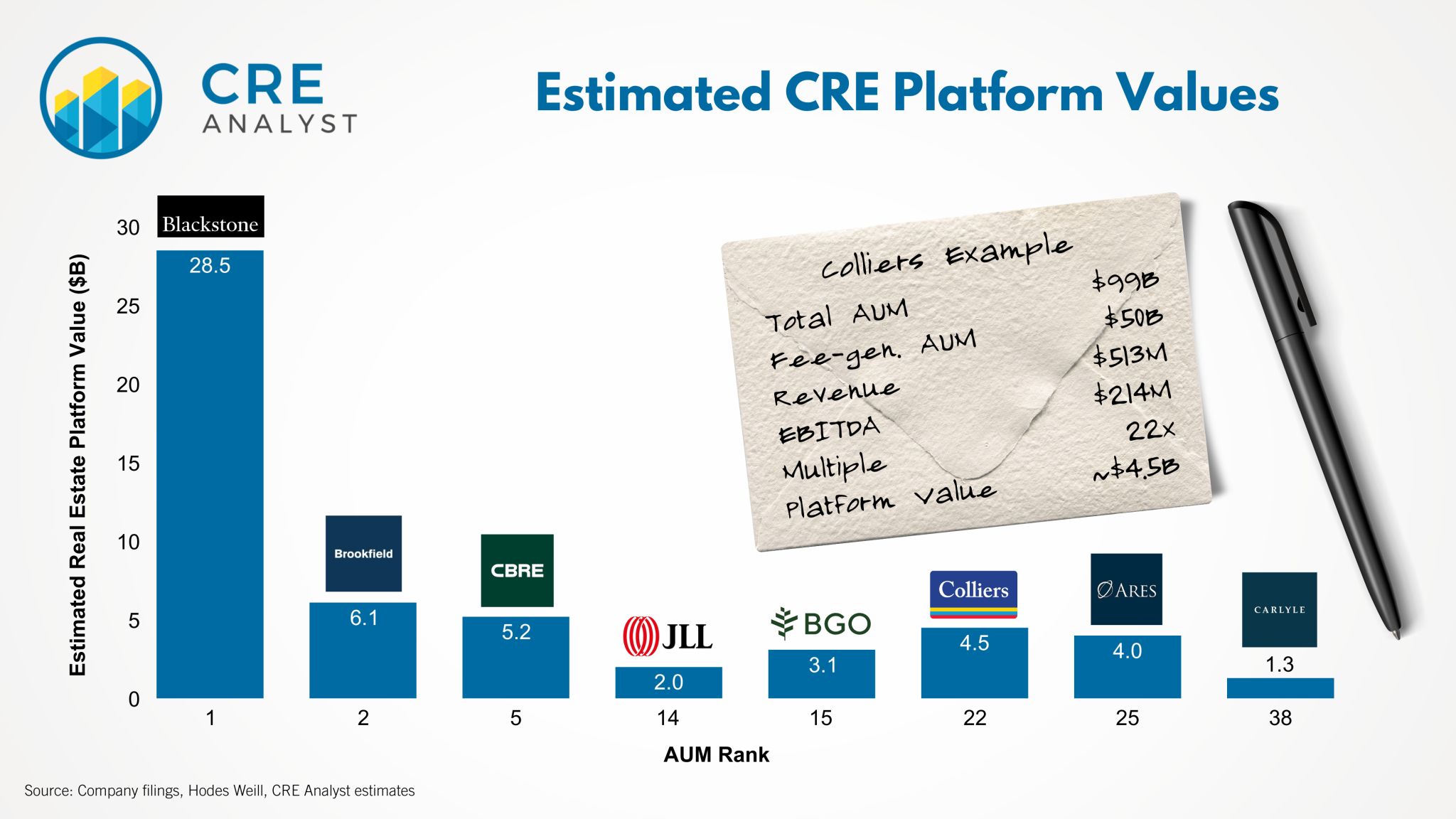

AUM is overrated. The real game is platform value.

Harder to measure, but it’s what drives strategy.

Our two cents...

1. Blackstone stands alone.

$339B in AUM, $279B in fee-AUM, premium multiple.

A category of one.

2. Margins matter.

JLL’s LaSalle runs at ~21% margin.

Colliers’ Harrison Street-driven platform at ~42%.

As AUM scales, margins expand, which makes allocators like Harrison Street and Blackstone powerful.

3. Fee-generating AUM > AUM.

Just look at Brookfield’s relative decline.

Private credit gets a lot of attention but core debt doesn't create much platform value.

4. Valuations swing.

Hodes Weill: 13x–20x earnings for platforms.

Why the gap? Durable, high-yielding funds command premiums.

5. Potential arbitrage?

CBRE IM: ~$5B value (~9% of enterprise).

Colliers IM: ~$4.5B (~40%).

Similar business, wildly different weightings.

How could they close the gap?

CBRE should:

-- Grow AUM immediately

-- Buy bolt-on managers

-- Diversify into infrastructure

-- Otherwise sell or IPO the investment management business

Colliers should:

-- Guard margins

-- Brand as a mini-Blackstone.

Sun Life should:

-- Leverage back door control of BGO

-- Sell to CBRE

Platform value shapes appetite.

Appetite shapes markets.

That’s why we follow the dollars.

Want to dig deeper? DM us to explore our upcoming FastTrack cohort.

COMMENTS