Trophy is the new class B?

Veris privatization winners and losers

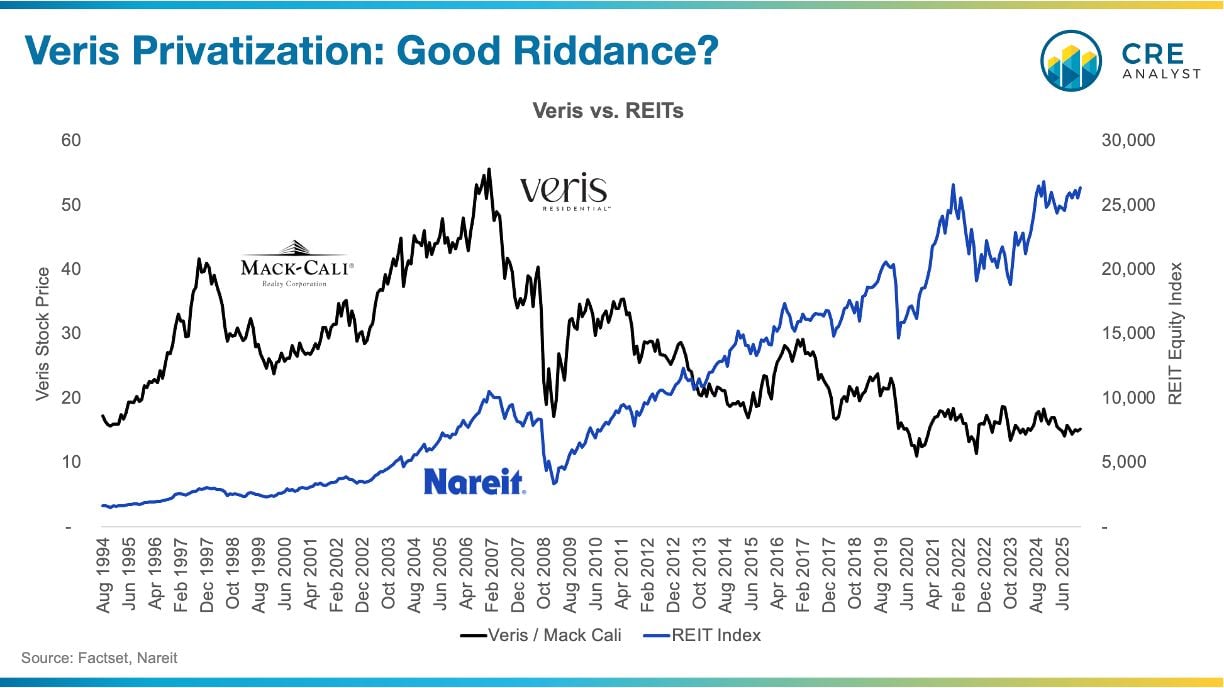

Veris Residential is finally going private.

30+ years as a public company.

...the REIT version of getting a first down when losing by 40 points.

(unless you're the CEO).

---- Kudos ----

The board deserves real credit. A new CEO took over in 2021, cleaned up the balance sheet, shifted the capital allocation strategy, and outperformed the apartment REIT index by 750 bps during his tenure.

The take-private represents a 25% premium to where the stock sat before an activist went public in December. For shareholders who stuck around, this is the best exit they were going to get.

---- What premium? ----

The buyer consortium, led by Affinius Capital and backed largely by GIC, is acquiring Veris at a mid-5% cap rate on the total portfolio.

That sounds fine until you compare it to what suburban apartments are pricing at: 5% or below for decently-located assets.

The luxury urban premium has effectively vanished.

---- Takeaways ----

Veris was an outlier: sub-scale G&A, looming debt maturities, and a portfolio that was hard to underwrite at scale. Most of the sector is fine.

But if you believe that luxury urban apartments are going to command the same appetite as down-the-middle residential assets, this deal is a data point probably gives you pause.

Buyers aren't paying up for trophy product right now. What a difference a few years make.

Winners:

-- Turnaround CEOs (will likely get huge payday)

-- Affinius and GIC

-- Activist investors

-- Boards that sell

Losers:

-- Long-term shareholders in small REITs

-- 'Trophy' multifamily (no premium)

-- Suburban office (sell occurred because REIT pivoted to multifamily)

-- Blackstone and Brookfield (less dominant buyers?)

COMMENTS