US CRE: High losses, slow burn

16 years ago Goldman Sachs put out a research piece that rattled real estate markets. Banks were sitting on mountains of toxic CRE debt, they said, which would throw a wet blanket over financials and take years to play out.

Sound familiar?

Key takeaways...

1. Slow burn:

Real estate credit challenges tend to play out over long periods. Even from the dire perspective of 2008, Goldman rightly predicted that losses would be incurred over years not months.

2. The devil is in the details:

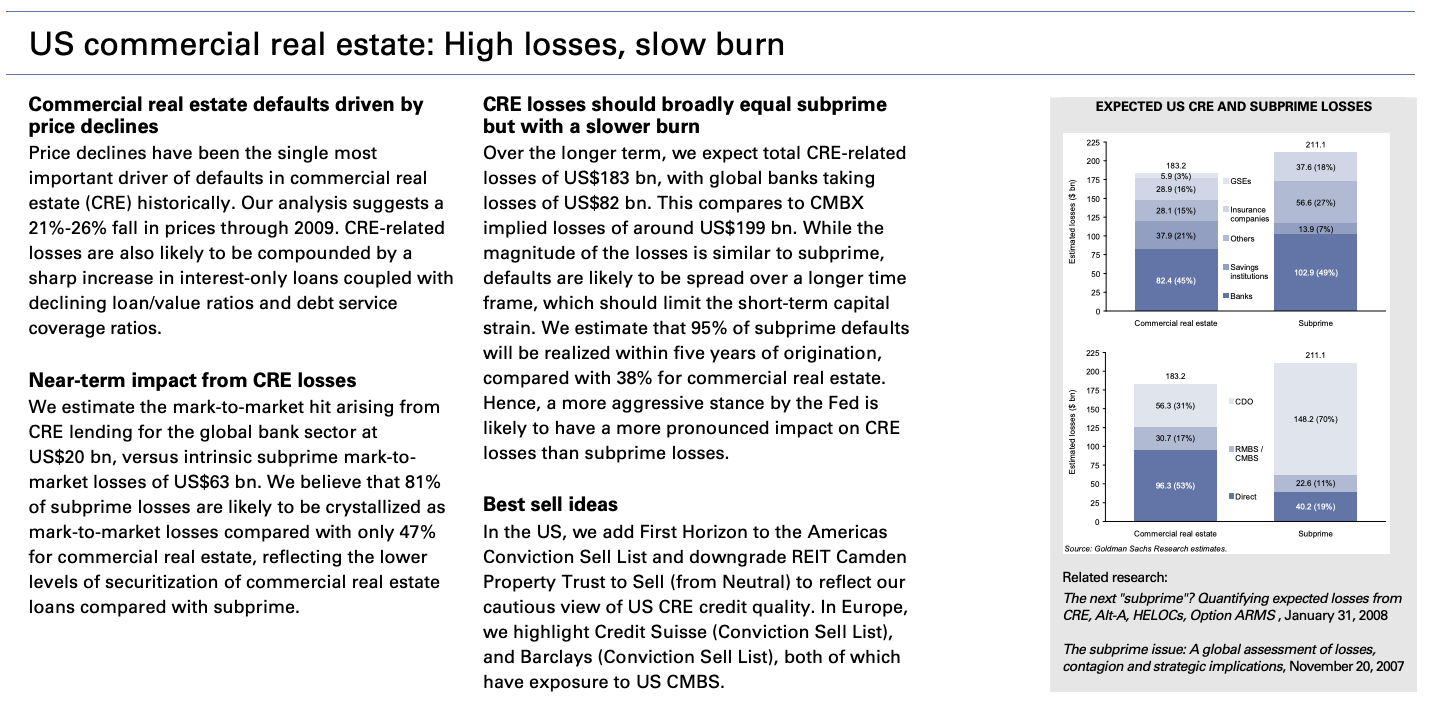

Goldman's analysis was based on top-down estimates. Their thesis: Values will fall, so defaults are coming. They then tried to allocate defaults and losses by lender type based on how aggressive the lenders had been in recent years.

Turns out, Goldman was right on some points (CMBS/CDO) and wrong on others (insurance companies). With CRE, the devil is in the details; bottom-up dynamics are almost always more insightful and actionable vs. top-down narratives.

3. Lending conditions were very different pre-GFC:

CMBS boomed. IO mortgages expanded from 23% to 86% of loan pools. Underwritten LTVs went from 65% to 70%. Underwritten DSCRs went from 2.3x to 1.6x. And the portion of CMBS pools rated AAA exploded from 67% to 88%. Much of this debt was packed and repackaged, increasingly calling more of it AAA for unsuspecting bondholders. Unsurprisingly, that paper imploded. Good news: This market is extremely different now. The riskiest lending is likely done in debt funds and mortgage REITs, where there is no AAA paper or expectations of pristine credit loss records.

PS - It's pretty easy for real estate pundits to get clicks and shares by talking about "doom loops," but there's an obvious divergence playing out in commercial real estate. The difference between winners and losers hasn't been this wide in decades and will almost certainly get more pronounced. Top-down narratives aren't as representative as they have been in recent decades. i.e., it's a lot harder to be a real estate reporter today than it was a few years ago. We'll keep trying to shed light on the nuances that define our industry. Let us know what you think we should dive into!

You can read the full article here!

COMMENTS