A year ago, everything was perfect. Commercial mortgages were plentiful and cheap. Transaction volumes were robust. Outlooks were rosy. Then everything changed. There are only three hazards that derail real estate cycles, and we’re clearly in the early stages of a hazard the industry hasn't faced in decades.

We've seen this before many times as the economy is either entering recession or in recession. The debt markets and the capital markets are rioting. ...this is an aberrant that happens one year out of every ten years, and we are either in the one year or about to go into the one year. - Steven Roth, CEO, Vornado

The Three Hazards of Commercial Real Estate

Hazard #1: Too much supply. This one is the biggest hazard. When supply outruns demand, the only two remedies are to demolish a lot of space (which rarely happens) or to wait until demand comes back to meet supply. The mid-1980s and early 1990s suggest that widespread oversupply can lead to rent, occupancy, and valuation declines that persist for up to a decade (even in "growth" markets). Thankfully, decision-makers are more informed than ever, which has mitigated the risk of widespread oversupply for the last 30 years.

Hazard #2: Too much debt. Occasionally, lenders get a new sports car, slam on the gas by lending too much, and eventually run off the proverbial road, often taking other financial markets with them. This level of recklessness tends to occur only once (ish) in a generation. A few examples: 27% of the CMBS loans originated in 2007 defaulted, 1,600 banks failed due to excess lending in the 1980s, and 80%+ of the real estate bonds floated in the 1920s failed to meet the terms of their loan contracts. As for today's debt levels, the shadow banking system has grown quickly since 2009, but debt funds represent only about 6% of the commercial mortgage market, so their ability to destabilize financial markets remains relatively muted. All other lenders, representing 90%+ of the market, are all regulated and reasonably constrained thanks to the 2007 hangover.

Hazard #3: Rising interest rates. This hazard, unlike the first two, isn’t self-inflicted but is especially cruel to real estate. And today, we find ourselves in the early stages of rising interest rate pain.

"There's plenty of capital. You just won't like the price. And that's true across the board." -Mark Gibson, CEO JLL Capital Markets (Americas)

No More Easy Money

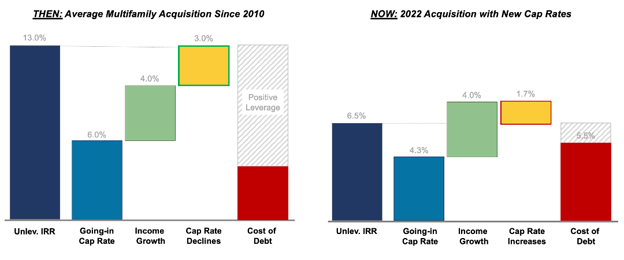

Let's say you bought a typical apartment property sometime over the last ten years. Market cap rates have averaged about 6%, which means you had income in year one equal to 6% of the purchase price. You also generated additional return by income growth (4% per year) and cap rate compression (every dollar of income was worth about 3% more per year thanks to more capital flooding into multifamily markets). Altogether, you could have generated about a 13% annual return before putting any debt on the property, and with 4% debt (the average cost of debt since 2010) you could have juiced your returns with leverage up to the mid/high teens. Easy money.

A comparative breakdown of returns looking backward (2010-2021) vs. looking forward

But if you were looking to buy that same multifamily property today, your going-in cap rate would probably be 4.25% to 4.75% (reflecting years of cap rate compression). And even if you benefited from a repeat of 4% annual income growth, cap rates expansion would mean you'll need to generate more income just to maintain today's valuation. You could pretty easily be left with a 6.5% unleveraged IRR, which doesn’t compare very favorably to 5.5% borrowing costs.

Why would investors take equity risk for a 6.5% return when they can get similar yields by investing in debt? How could a property heading into a meaningful recession generate 4% income growth per year? Why would a lender or a buyer invest in an asset that is sinking in value even as its NOI increases? No one has great answers to these questions, which is why sales volumes have slowed by about 50%.

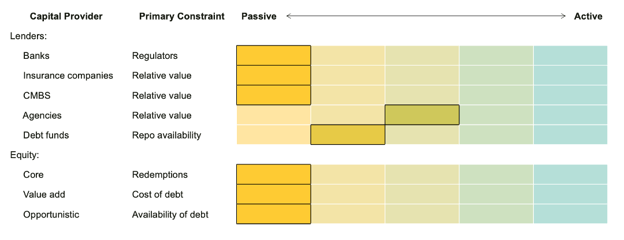

Capital Markets Scorecard

The following chart reflects our anecdotal understanding of how active (or inactive) capital providers are as of Nov/Dec 2022.

This reflects our general take on the eight primary capital providers.

Public vs. Private Real Estate Pricing

If you own a piece of real estate, you probably didn’t buy it yesterday and likely won’t be selling it tomorrow, regardless of what someone says it’s worth or not worth. Private assets just don’t trade that often, which leaves us to guess what they’re worth. This guessing game takes time, so reality inherently lags behind our guesses.

But you could also own shares of public real estate companies, and you could buy and sell them multiple times a day. Suppose you read a negative article about office buildings, you might sell ESRT. Or if you stumbled on an 18-second YouTube video promoting self-storage, you could buy NSA. [Note: We randomly selected those examples and don’t provide investing advice.]

Given this difference in the short-term drivers of public and private markets, there’s often a disconnect between public and private values. In fact, public markets tend to lead private values, and sometimes the value of an individual property company (REIT) can get significantly out of whack, leading to activist investor campaigns.

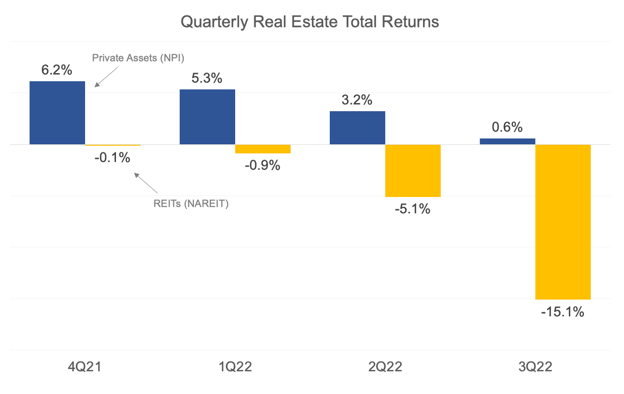

Quarterly Real Estate Returns over the Last Year

REIT values have declined substantially in recent months, while private asset values have moderated much slower.

Returns for private assets (as measured by NCREIF's core property index) averaged 16.1% over the last year. Not bad at all. But REIT returns have fallen by nearly 20% over the last year. Although public markets may be leading private markets (the NCREIF Property Index is based, in part, on trailing appraisals), the differences are more pronounced for some companies.

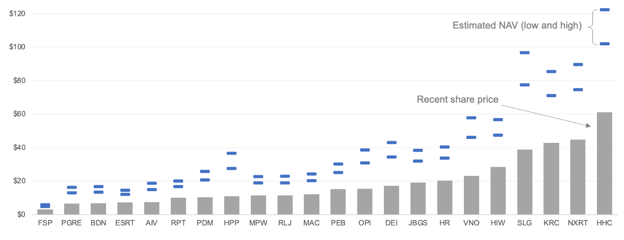

Our rough estimates suggest that these 22 stocks trade 45% to 55% below asset values. Note that we don't own any of these stocks and don't offer investment advice. This is presented to illustrate the differences between real estate in the public and private markets.

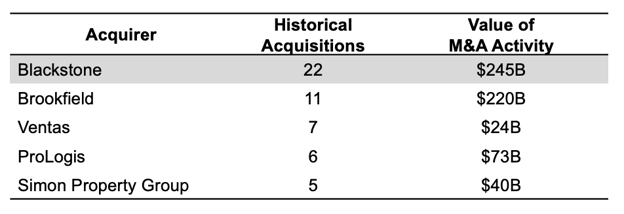

Historical REIT M&A Transactions

When REIT values nose dive or private values skyrocket, savvy investors exploit pricing differences by buying discounted publicly-traded real estate companies. They typically have to pay a hefty premium over current stock prices, but on occasion, the math works. To be clear, it takes a special sort of firm to exploit these differences (corporate takeovers don't fit well into most fundraising pitch decks), but two firms, Blackstone and Brookfield, have consistently tapped the public markets for acquisition opportunities.

Blackstone and Brookfield have dominated REIT M&A activity over the last 15 years.

Brookfield just raised a massive fund but no firm has more experience in this space or more dry powder than Blackstone.

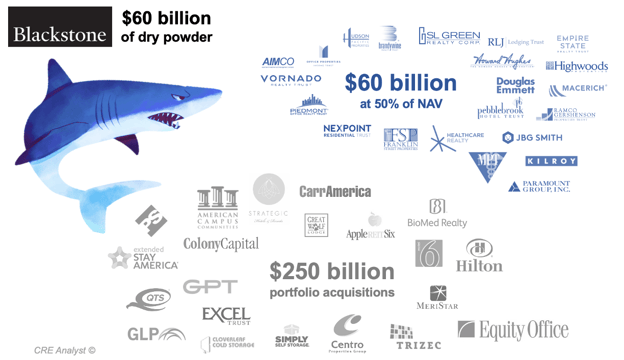

An Obvious Buyer?

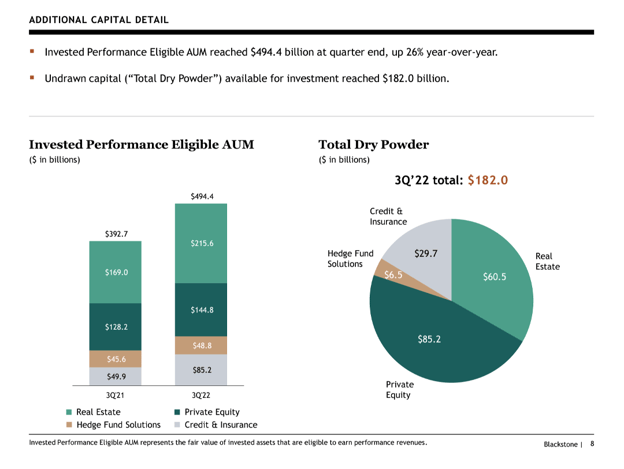

After several quarters of remarkable fundraising feats (i.e., pulling in an average of $17 billion a quarter since 2020), Blackstone sits on more than $60 billion of real estate "dry powder."

According to Blackstone's most recent quarterly report, the firm sits on $182 billion of total dry powder, which includes more than $60 billion in real estate capital that is primed to be deployed.

"If there is a slowdown in market activity, we can afford to be a little patient, and then when opportunity emerges, we can move." - Jonathan Grey, COO, Blackstone

Green shoots and next steps

1. Most large real estate firms (owners, lenders, and brokers) are in a far better capital position today than in the financial crisis. Widespread distressed sales seem unlikely.

2. Some capital providers are poised to re-enter the market relatively quickly. Banks are sitting on record levels of cash, and many insurance companies and agencies restart annual targets in the new calendar year, which could provide a relative kickstart to transaction activity. Additionally, many value-add and opportunistic equity funds are sitting on significant undrawn capital; they just need borrowing rates (or acquisition prices) to cooperate in order to facilitate more transactions.

3. Higher interest rates affect all asset classes. Therefore, we could be amid a settling period, where high-quality commercial real estate--a relative hedge against inflation--ends up a relative winner over the intermediate term.

COMMENTS