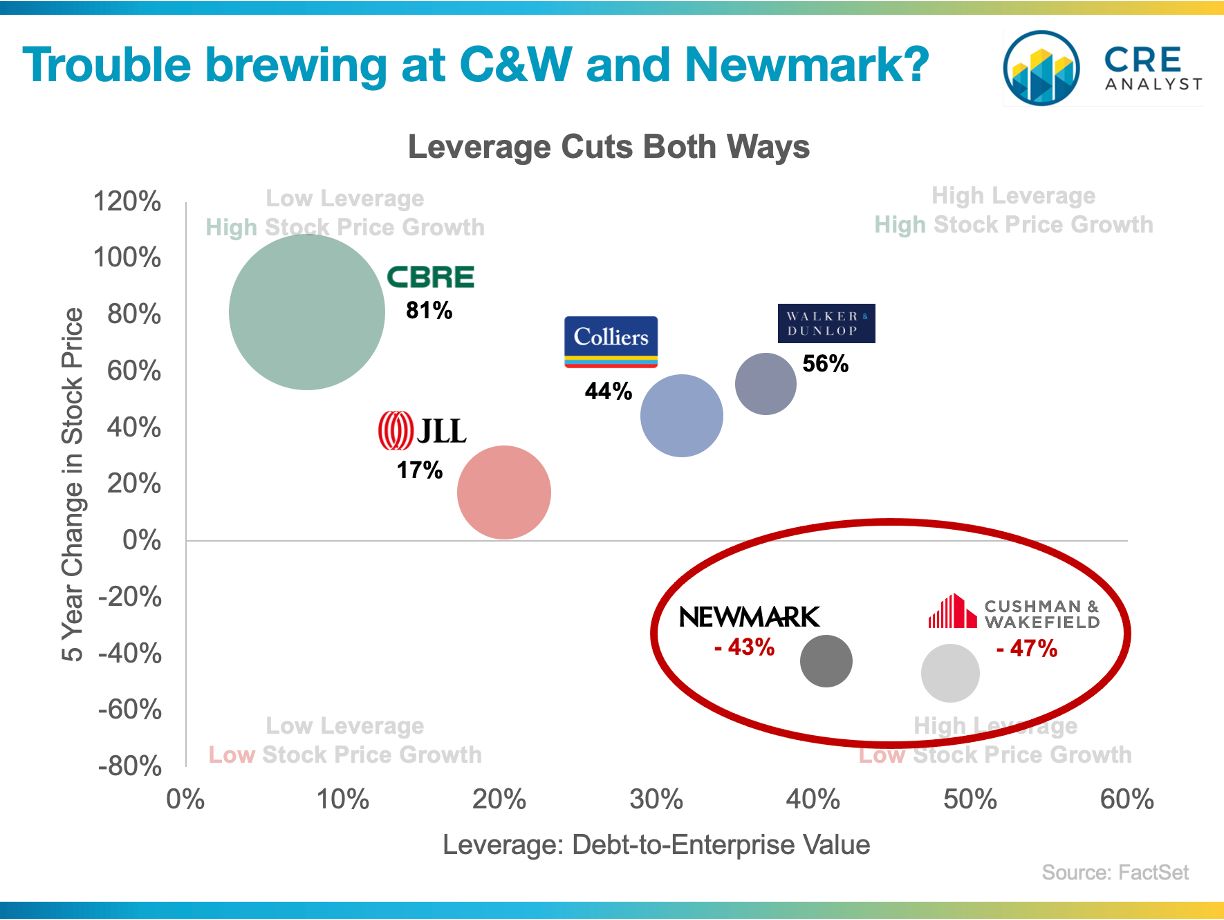

Leverage cuts both ways: Brokerage edition

----- Cushman & Wakefield -----

C&W's new CEO Michelle Mackay seems to be trying to take a page out of Bob Sulentic's playbook. Sulentic substantially deleveraged CBRE over the last ten years and turned CBRE into a cash flow machine (CBRE is sitting on about $1.4B of cash*). But Mackay is working with a very different hand.

C&W issued $400M of senior debt last month at 8.875%. Despite borrowing less than its maturing senior debt, its cost of borrowing increased by more than 30%. C&W simultaneously refinanced a $1B term loan at 9.3%, which represented a 3x increase in relative borrowing cost.

The firm's all-in cost of debt is about 8% vs. an operating margin of 8.9%. i.e., C&W is handcuffed by its lack of free cash flow.

----- Newmark -----

Similarly, Newmark reported a 12% operating margin last quarter, and--like C&W--is grappling with higher interest costs. Newmark recently announced that it would refinance about half of its maturing $550M of senior bonds with new bonds priced at 7.9% (a 30% increase in cost) and the other half with its revolver and cash. Newmark's revolver, which increased in cost from about 3% to nearly 7% over the last 18 months, is scheduled to mature in 1Q 2025.

----- Takeaways -----

Will C&W or Newmark go out of business? Probably not.

Are either in a position to make bets on expansion? Not likely.

Will key brokers get poached? Probably.

Notice a theme to leverage? Debt magnifies returns and volatility. Investors and managers often talk about debt as if it only makes returns better, but they rarely discuss how debt can sideline or kill companies when ROI is the highest.

----- P/E multiples -----

Investors perceive risk and demand to get paid for it. In a business like brokerage, where revenues swing wildly, investors tend to pay up for safety. This is a real-time example of how there's no greater magnifier of risk than debt...

Newmark trades at 8x earnings and Cushman trades at 9x.

JLL at 18x and CBRE at 20x.

i.e., the same $ of income is worth 2x more at JLL or CBRE.

From a capital structure perspective, C&W and Newmark seem stuck and at a meaningful disadvantage to their peers.

----- CBRE follow-up -----

* CBRE is sitting on a ton of cash, but it has a different problem. Relatively low returns on that cash have left significant value on the table. A much better problem to have than being handcuffed by debt, but a problem nonetheless.

COMMENTS