When safer is riskier: "Stabilized core" at $400M or buy broken at $125M?

A case study on how a real estate private equity fund played the property clock perfectly.

---- Background ----

Ten years ago, the Taj Boston was an iconic but tired full-service hotel in Boston's Back Bay.

Originally opened as the Ritz-Carlton in 1927.

Six ownership groups by the time of the 2016 sale.

By then the building was nearly 90 years old, the brand no longer competed with the Four Seasons or Mandarin Oriental nearby, and operations had drifted under absentee international ownership.

---- Acquisition ----

July 2016: A partnership led by New England Development and Eastern Real Estate, with Rockpoint Real Estate Fund V as institutional capital, acquired the hotel off-market for $125 million.

Rockpoint's deck framed the underwriting as "an iconic hospitality asset...at an attractive basis relative to stabilized cash flow, and at a significant discount to both replacement cost and recent comparable sales."

The plan: a targeted capital improvement plan to reposition a well-located but outdated hotel.

---- Execution ----

What actually happened in the 21-month hold was narrower than the underwriting implied.

Rockpoint replaced the management company at close, stripped ~$4 million of annual operating expenses, engaged an architect to resolve constraints that had stopped prior owners from delivering a five-star product, and delivered three model rooms in Q2 2017 to showcase the upside.

Then they sold.

April 2018: $203 million. More than 21 months ahead of plan. Rockpoint retained a passive equity stub with a liquidity mechanism tied to stabilization.

The next owner closed the hotel in October 2019, gut-renovated under the Newbury Boston brand with Highgate operating, and reopened in May 2021.

---- Takeaways ----

Rockpoint sold the dream well before the pandemic. The Newbury is now a five-star hotel commanding $1,000+ per night.

How would the next owner have fared buying the Newbury at a stabilized market cap rate in 2021?

Who has more downside: the buyer of a broken hotel at $125M, or the buyer of a "stabilized" hotel at a 6% cap rate?

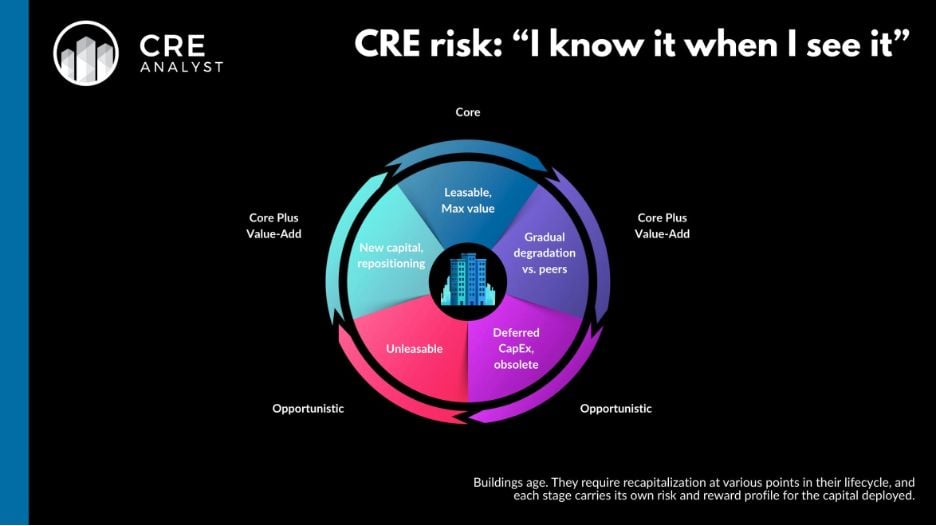

Buildings aren't lines on spreadsheets.

PS -- This is a good example of how we turn the messy world of real estate into actionable frameworks. Get our insights in your inbox by subscribing at creanalyst.substack.com.

A case study on how a real estate private equity fund played the property clock perfectly.

---- Background ----

Ten years ago, the Taj Boston was an iconic but tired full-service hotel in Boston's Back Bay.

Originally opened as the Ritz-Carlton in 1927.

Six ownership groups by the time of the 2016 sale.

By then the building was nearly 90 years old, the brand no longer competed with the Four Seasons or Mandarin Oriental nearby, and operations had drifted under absentee international ownership.

---- Acquisition ----

July 2016: A partnership led by New England Development and Eastern Real Estate, with Rockpoint Real Estate Fund V as institutional capital, acquired the hotel off-market for $125 million.

Rockpoint's deck framed the underwriting as "an iconic hospitality asset...at an attractive basis relative to stabilized cash flow, and at a significant discount to both replacement cost and recent comparable sales."

The plan: a targeted capital improvement plan to reposition a well-located but outdated hotel.

---- Execution ----

What actually happened in the 21-month hold was narrower than the underwriting implied.

Rockpoint replaced the management company at close, stripped ~$4 million of annual operating expenses, engaged an architect to resolve constraints that had stopped prior owners from delivering a five-star product, and delivered three model rooms in Q2 2017 to showcase the upside.

Then they sold.

April 2018: $203 million. More than 21 months ahead of plan. Rockpoint retained a passive equity stub with a liquidity mechanism tied to stabilization.

The next owner closed the hotel in October 2019, gut-renovated under the Newbury Boston brand with Highgate operating, and reopened in May 2021.

---- Takeaways ----

Rockpoint sold the dream well before the pandemic. The Newbury is now a five-star hotel commanding $1,000+ per night.

How would the next owner have fared buying the Newbury at a stabilized market cap rate in 2021?

Who has more downside: the buyer of a broken hotel at $125M, or the buyer of a "stabilized" hotel at a 6% cap rate?

Buildings aren't lines on spreadsheets.

PS -- This is a good example of how we turn the messy world of real estate into actionable frameworks. Get our insights in your inbox by subscribing at creanalyst.substack.com.

COMMENTS