When "worst case" looks good: welcome to the Class B multifamily reset

Here's an apartment syndicator's Adam Neumann-like description of cap rates from a 2022 PPM:

"While acquisition cap rates are not irrelevant metrics, they may be considered less important in this case; the partnership is not buying the Project for its historical or in-place NOI and cash flow, but rather for its potential to earn higher NOI in the future."

Translation: in-place NOI is overrated.

----- Why this matters now -----

S2 Capital is back in the headlines because many of their investments have reportedly gone to zero. The quote above isn't from S2 directly. It's from Trinity, the feeder that raised LP capital for S2 and just told investors to expect a loss.

Again, this quote isn't from S2. It's from ANOTHER sponsor that Trinity funnelled money to. Trinity invested ~$1.2B in 2021-22, and class B multifamily was a favorite target.

There's a lot more where S2's problems came from. Same vintage. Same playbook. Same conviction that in-place economics didn't matter because the curve only bent one way.

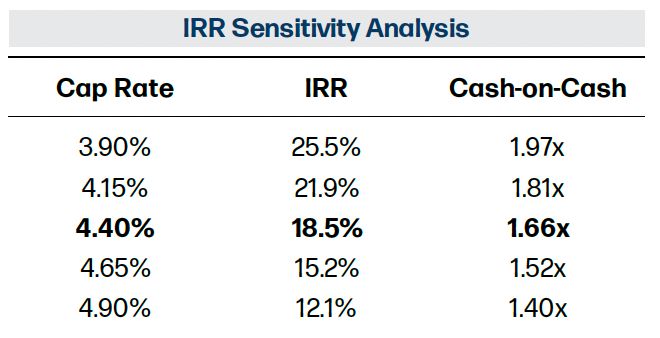

The same PPMs that waved off in-place income also included "worst case" sensitivity tables. Those worst cases now look like upside fantasy dreams now.

----- The bigger point -----

This isn't about throwing shade. Everyone makes mistakes.

But there are axioms in our business that get conveniently ignored when incentives are misaligned. The frameworks of our business matter, even when syndicators ignore them to raise money. These faults cause real problems for real people. Worth spotlighting.

PS -- More detailed analysis on our Substack.

COMMENTS