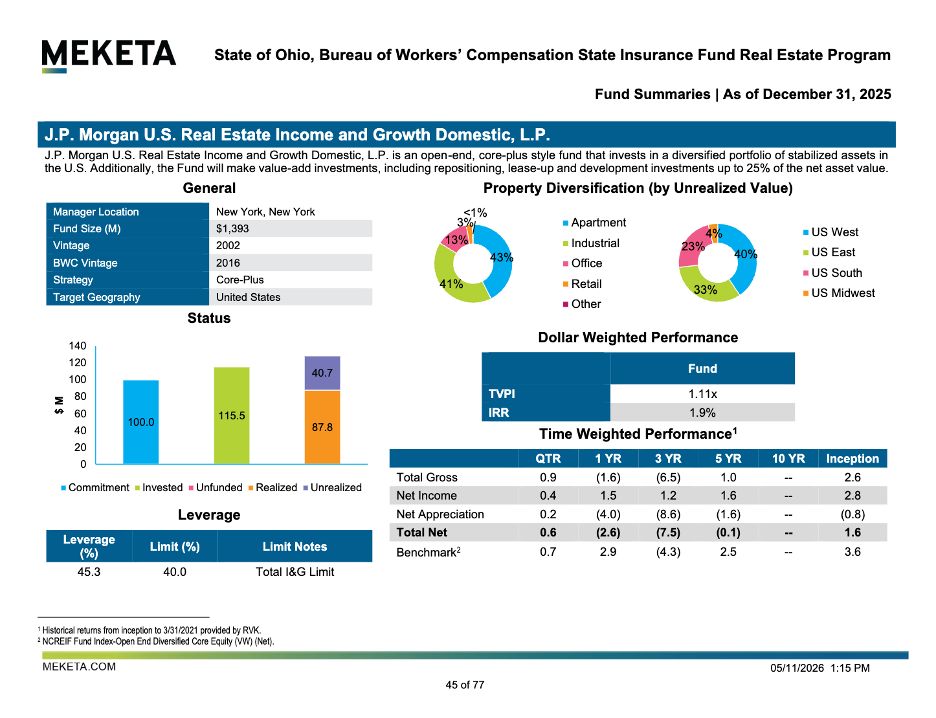

JPM is shutting down a billion-dollar real estate fund because...

---- Quick background ----

Buried in a recent pension fund report:

“J.P. Morgan announced starting April 13, 2026 the U.S. Real Estate Income and Growth Fund will begin a wind-down of the Fund. ...asset management fees will be reduced during the wind-down, which is anticipated to take up to three years.”

---- Likely rationale ----

1. Scale: It was ~$1.9B in 2010 and is ~$1.4B now.

2. Strategy: The core plus benchmark only returned 3.6% over 25 years. Not great.

3. Underperformance: < 2% IRR

Best guess: office and leverage didn't pan out as expected, recent cap rate expansion stings.

4. Economics: 105 bps fee

Forget 2 and 20. JPM charges 75-105 bps to manage this vehicle. Hard to make these tight fees work under $5-10 billion of AUM.

---- Context ----

The core and core plus fund space has evolved in very interesting ways over the last 10+ years.

What was supposed to be the safest strategy ended up being the riskiest after rates spiked. Performance has been lackluster across the board (even Blackstone's core plus fund has only generated a 3% IRR). Plus, there's been very little liquidity in institutional perpetual funds.

With values having stabilized, ODCE core funds are competing with dozens of smaller funds that have emerged with less reliance on being in the benchmark and more of a focus on betting the benchmark via speciality asset classes.

Some examples:

-- Invesco's core plus fund has outperformed by underweighting heavy capex sectors (office) and integrating niche operators.

-- Kayne Anderson's core plus fund has outperformed by betting big on medical office.

-- Harrison Street's core plus fund has outperformed by betting big on student housing and storage.

-- Carlyle's core plus fund has outperformed by being significantly overweight in manufactured housing, SFR, medical office, and active adult.

---- Takeaways ----

This fund wasn't a shiny new toy for JPM. It was launched 20+ years ago. Maybe it was a vehicle caught in no man's land. If so, it wouldn't be alone.

Our industry is probably in the early stages of unwinding vehicles, roles, and strategies that were well-intentioned but lack a tailwind or clear competitive advantage.

---- Quick background ----

Buried in a recent pension fund report:

“J.P. Morgan announced starting April 13, 2026 the U.S. Real Estate Income and Growth Fund will begin a wind-down of the Fund. ...asset management fees will be reduced during the wind-down, which is anticipated to take up to three years.”

---- Likely rationale ----

1. Scale: It was ~$1.9B in 2010 and is ~$1.4B now.

2. Strategy: The core plus benchmark only returned 3.6% over 25 years. Not great.

3. Underperformance: < 2% IRR

Best guess: office and leverage didn't pan out as expected, recent cap rate expansion stings.

4. Economics: 105 bps fee

Forget 2 and 20. JPM charges 75-105 bps to manage this vehicle. Hard to make these tight fees work under $5-10 billion of AUM.

---- Context ----

The core and core plus fund space has evolved in very interesting ways over the last 10+ years.

What was supposed to be the safest strategy ended up being the riskiest after rates spiked. Performance has been lackluster across the board (even Blackstone's core plus fund has only generated a 3% IRR). Plus, there's been very little liquidity in institutional perpetual funds.

With values having stabilized, ODCE core funds are competing with dozens of smaller funds that have emerged with less reliance on being in the benchmark and more of a focus on betting the benchmark via speciality asset classes.

Some examples:

-- Invesco's core plus fund has outperformed by underweighting heavy capex sectors (office) and integrating niche operators.

-- Kayne Anderson's core plus fund has outperformed by betting big on medical office.

-- Harrison Street's core plus fund has outperformed by betting big on student housing and storage.

-- Carlyle's core plus fund has outperformed by being significantly overweight in manufactured housing, SFR, medical office, and active adult.

---- Takeaways ----

This fund wasn't a shiny new toy for JPM. It was launched 20+ years ago. Maybe it was a vehicle caught in no man's land. If so, it wouldn't be alone.

Our industry is probably in the early stages of unwinding vehicles, roles, and strategies that were well-intentioned but lack a tailwind or clear competitive advantage.

COMMENTS