It sounded like a great idea at the time...

Buy apartments. Use cheap floating-rate bridge debt. Push rents. Refi in 18 months. Repeat.

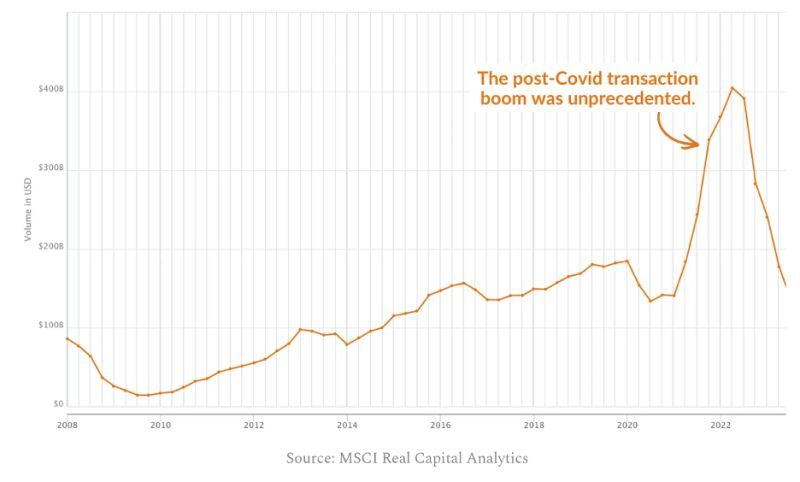

From 2021 into early 2022, transaction volume went vertical, peaking near $400B. Apartments were the engine. Nothing in the prior 40 years looks like it.

It was a perfect storm:

Rents were ripping, 10%+ growth across the Sun Belt.

Cap rates kept compressing, so every deal "worked" on paper.

Fulcrum 1: Cheap debt

Bridge debt was cheap with SOFR near zero.

But then SOFR ran from ~0% to 5%+.

Floating debt that penciled around 3.5% reset around 8%+.

Rate caps that cost a syndicator $30k in 2021 cost $1M+ to renew.

The refi that was supposed to bail everyone out went from friend to enemy.

...especially when rent growth flattened.

Fulcrum 2: Equity syndicators

They raised retail equity in $100K chunks.

They bought at the top and signed for the bridge loan.

Expiring rate caps were the first dominoes.

Why'd they do it? Syndication fees probably helped. The returns looked great.

Our recent Substack deep dive pulls back the layers on how syndicators fueled much of this historic apartment boom.

...but their role or the fact that equity gets wiped in a downturn weren't huge surprises.

The biggest surprise from our analysis?

How the lenders who fueled the boom are performing.

It's easy to hide behind "kicking the can" narratives or the fact that CLOs sound like CDOs.

But the reality (so far) paints a relatively favorable picture of the debt behind the last cycle's most aggressive deals.

COMMENTS