Seth Klarman wrote the book "Margin of Safety." Then he lost a Houston office tower to the lenders.

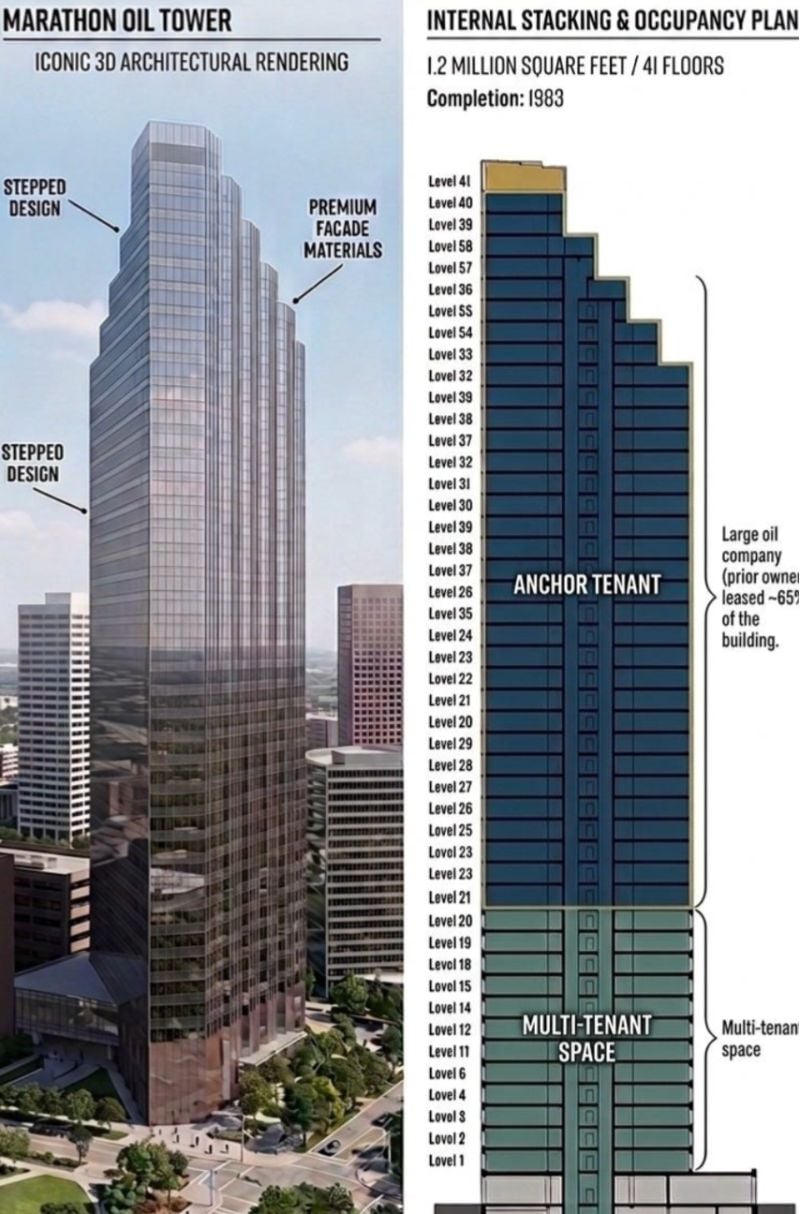

In 2013, CBRE Investment Management paid ~$250 million for Marathon Oil Tower, a 1.2 msf office building in Houston. Marathon Oil, the anchor tenant, leased ~65% of the space.

The whole deal came down to one question: does the anchor renew?

If Marathon stayed, the tower was worth ~$325 million. If Marathon left, it was worth under $90 million.

No middle. No "average" outcome. Stay, and the sponsor makes ~$75 million.

Leave, and the sponsor loses everything.

----- This is the shape lenders fear -----

Equity gets to be wrong a lot, because it only needs to be right occasionally. One winner pays for forty zeros.

Lending is the mirror image. Best case is your money back, par plus a spread.

You often can't earn your way out of a loss, because the upside that funds the comeback was never yours. One bad loan eats the spread off ten good ones.

So the entire job reduces to one question: how do I avoid losses?

A binary asset like Marathon Tower is the nightmare version. The downside is vaporization.

----- Then it got interesting -----

Marathon left. CBRE shopped the building and eventually sold it to Baupost and a local operator for $177 million.

Baupost's CEO is Seth Klarman. He literally wrote "Margin of Safety: Risk-Averse Value Investing Strategies for the Thoughtful Investor." Used copies sell for a few thousand dollars.

$177 million looked like margin of safety. Down from the ~$250 million CBRE paid. Way down from the ~$325 million bull case. A disciplined, downside-obsessed buyer stepping in at a discount.

Within a few years, Baupost handed the keys to its lenders, who foreclosed on $90 million of debt.

----- The lesson -----

There is no "good basis" when outcomes are binary. Klarman's team didn't misjudge the upside. They misjudged the floor.

If the most disciplined value investor alive, the man who wrote the definition of downside, can misread basis and downside on a single building, you understand why a lender pricing that same building gets skittish.

Spread compensates you for risk across portfolios. It doesn't save you from risk. On an asset that can fall to $90 million, no coupon is high enough. The only real protection is structure, and structure is the first thing competition takes away.

Bottom line: lenders aren't paranoid. They've just done the arithmetic. In credit, you only get to be surprised to the downside.

Remember this next time you get mad at your lender.

PS -- want a better understanding of what differentiates real estate capital? DM us to explore joining our Fall FastTrack cohort.

COMMENTS