Private credit was supposed to be the safe bet.

It's playing out backwards.

Senior. Secured. Floating rate. First in line. That was the pitch. Commercial real estate, by contrast, was the asset class everyone was told to fear.

Watch how it's actually sorting out.

----- Two deals, same playbook -----

In 2021, a Blue Owl-led group financed Vista's take-private of Pluralsight. The software firm's EBITDA couldn't carry the debt, so lenders underwrote the subscription line and priced it at SOFR + 800.

In 2022, Tides bought an old Class B apartment complex at a 3.5% cap. 92% loan-to-cost. Roughly 7%, about 600 over SOFR. Floating. Due in three years.

One lender bet on ARR growth. The other bet on rent growth. Both loans floated. Both were on the clock. Both sponsors got wiped out.

----- Different recoveries -----

Pluralsight's lenders are marking losses. Vista already took the equity to zero, and the debt is scattered across BDCs all over the system.

Tides' lenders are treading water. The loan funded at ~$148K/unit. The property still throws off $14-15K/unit/year, and the lowest Austin comp in two years implies a value of ~$144K/unit. That's a ~3% haircut, not a wipeout.

One had collateral you can live in. The other had collateral you can cancel.

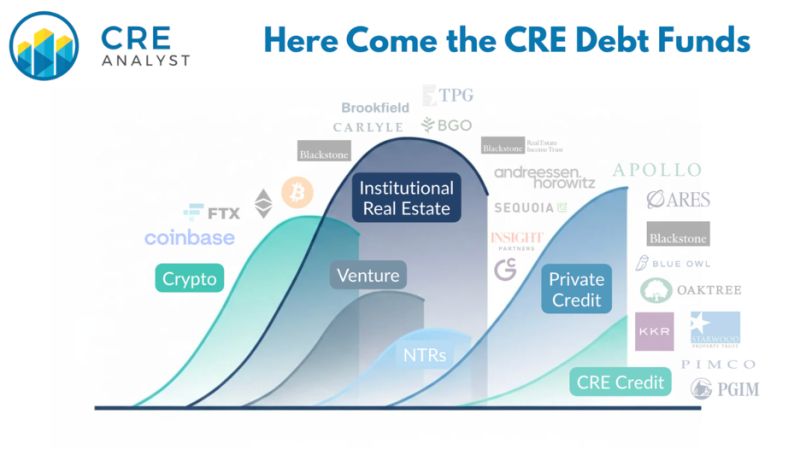

Bottom line: the risk was never in the label. It was in the collateral. Big platforms are leaning hard into this reality.

KKR just closed $1B for its latest opportunistic real estate credit fund, and Blackstone launched Brio.

When Jon Gray gets asked about real estate and answers in credit, that's not a pivot. It's a verdict.

Check out KKR's deck, Brio details, and detailed commentary/analysis at our Substack page.

COMMENTS