Everyone wants to fund digital infrastructure.

No one wants to fund real estate.

These two may be more related than they look.

Ask anyone why real estate feels so quiet and they start with interest rates.

But there is another answer that increasingly gets overlooked:

Infrastructure is crowding real estate out of the capital stack.

---- Follow the dollars ----

1. Scale

It is hard to hold this one in your head. Nvidia is worth roughly $5 trillion, which is about the size of the entire institutional U.S. real estate market.

AvalonBay and Equity Residential just merged into the largest apartment owner on earth, a roughly $69 billion company. Nvidia throws off enough cash in a few quarters to write that check outright.

Who had ever heard of NVIDIA three years ago?

2. The build

For the first time on record, the U.S. is spending more building data centers than offices. And the boom is speeding up, not settling down.

About 27 gigawatts of data-center capacity broke ground globally last year, the most active year ever. The pipeline behind it is more than 240 gigawatts. Roughly eight times that record (MSCI).

3. Where the money comes from

Part of it is the hyperscalers themselves, plowing most of their cash flow into these projects. The four biggest are spending on the order of $400B this year and $600B+ next.

But investment managers are all over it too, led by Blackstone, and the early reads on these plays are good.

---- Pension fund example ----

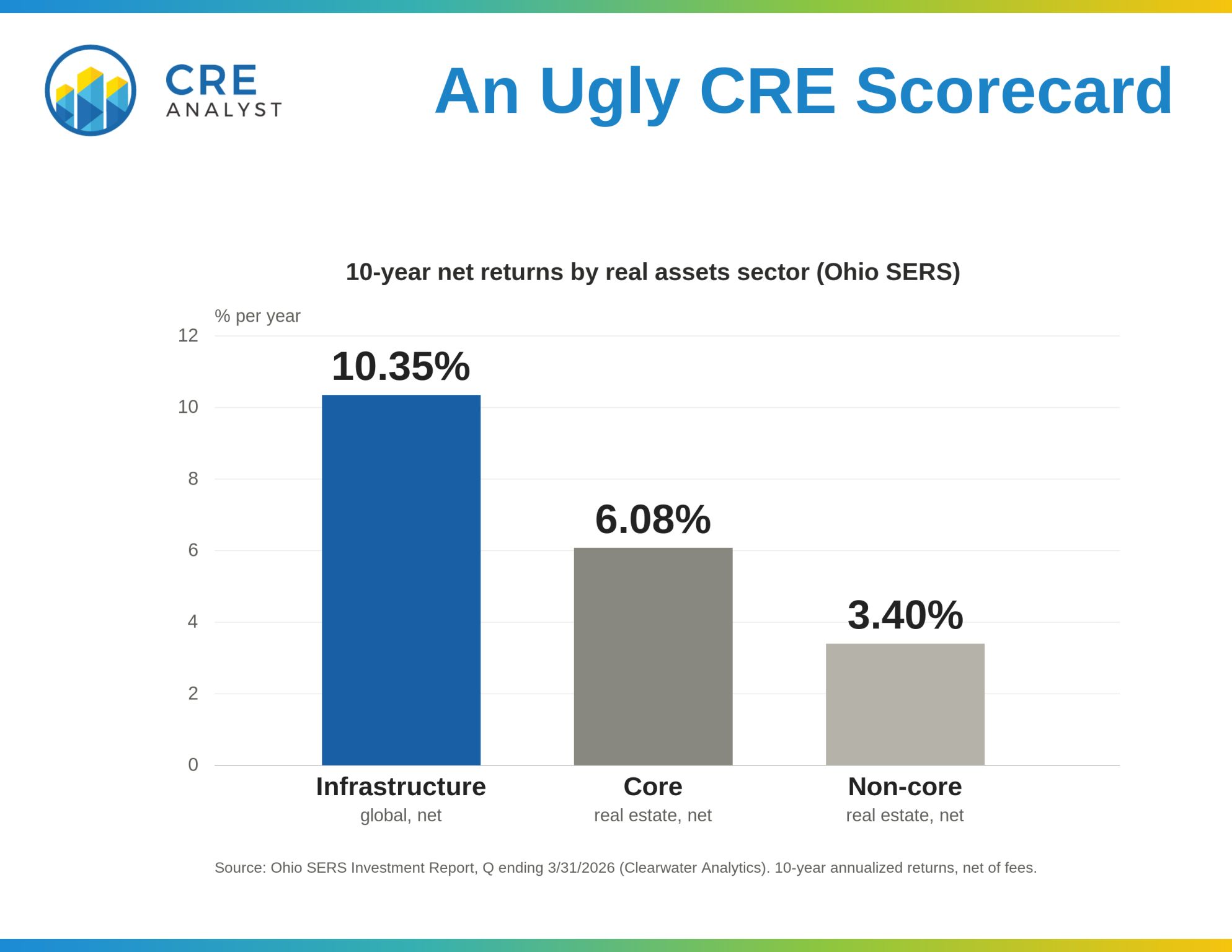

Last month the School Employees Retirement System of Ohio reviewed its asset allocations, with an intense focus on ‘real assets’ which holds both real estate and infrastructure.

The real estate staffer went to the mic first. Real estate is about 10% of the fund, worth $2.2 billion. Recent returns trailed the benchmark by 130-plus basis points, and the team had just taken $125 million in redemptions.

Then the infrastructure staffer stepped up. Infrastructure is 7% of the fund, worth $1.6 billion, returning 10% net last year and beating its benchmark by 200 basis points, after 300 and 600 basis points of outperformance the prior years.

Here's what the board saw...

Ten-year returns:

-- Core real estate: 6%

-- Non-core real estate: 3%

-- Infrastructure: 10%

Any guesses as to what the board did next?

They cut real estate’s allocation in half.

Assume the board is wrong.

Assume they are chasing the shiny toy, caught up in the hype around AI and data centers.

Or assume they just made bad real estate investments.

---- Takeaway ----

Real estate used to compete with other real estate for capital. Now it competes with the largest, most aggressive bid in the history of markets. And on the only scoreboard that actually funds deals, it is losing.

That is the part interest rates do not explain.

COMMENTS